When Can I Give Further Advice (ROA’s)?

Quite often (very often), we get calls from advisers wanting to go through a scenario to see if they need to give their client an SOA or an ROA.

This article will address some of the issues to consider and how to go about approaching the SOA vs ROA conundrum.

When can I give an ROA?

There are 3 separate advice situations where an ROA can be used, but the main scenario is as follows:

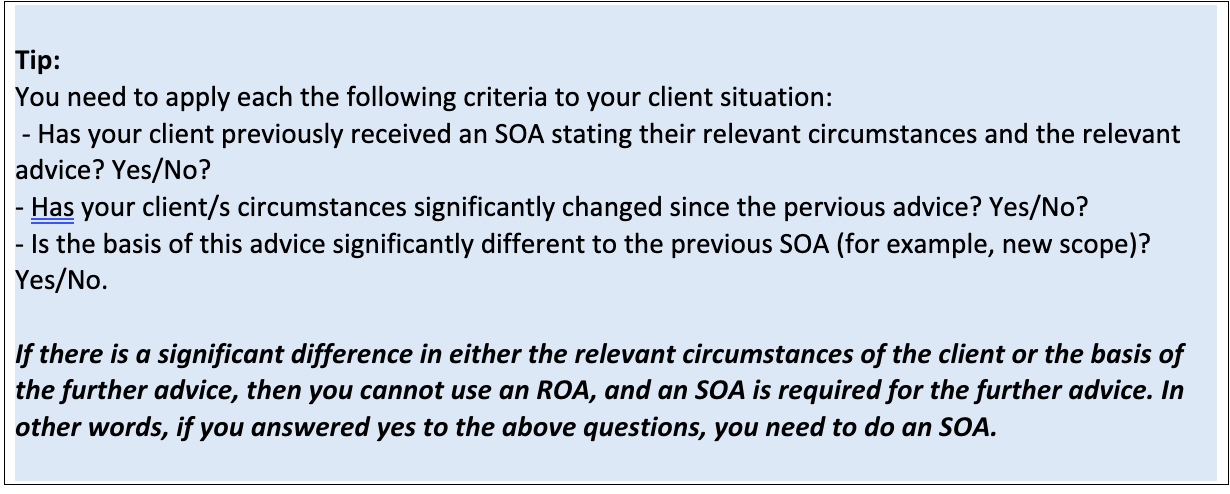

You can give further advice to the client, when:

you have previously given the client an SOA setting out the client’s relevant circumstances in relation to the advice (the ‘previous advice’)

the client’s relevant circumstances in relation to the further advice are not significantly different from when the client received the previous advice, and

to the extent the further advice is based on matters other than the relevant circumstances of the client – the basis on which the further advice is given is not significantly different from the basis on which the previous advice was given: see reg 7.7.10AE.

When applying your client scenario to the above criteria, ASIC encourages advisers to use their professional judgement.

Using your professional judgement

The legislation and guidance do not cover each and every possible client scenario of when it is appropriate to use an ROA. Therefore, you need to use your professional judgement.

Often, when we get calls with these scenarios, the adviser will preface the conversation and say ‘I am pretty sure I know the answer, but just want to run it past you”. OR “We know we need to do an SOA, but hoping you can tell us otherwise”.

You are experienced professionals. You understand the client scenario, the previous advice and the legislative requirement. We would encourage you to use your professional judgment when applying your client scenario to the above criteria.

What is a significant change in circumstances?

If the client’s relevant circumstances at the time you provide further advice are significantly different from the circumstances that you considered when providing the previous advice, you cannot use an ROA and must give the client an SOA for the further advice: see regulation 7.7.10AE(2)(b).

You will need to exercise your professional judgement when considering whether any of your client’s relevant circumstances are significantly different from when the previous advice was given.

Examples of relevant circumstances that may be considered significantly different include:

a new mortgage or significant increase or decrease in debt

divorce or separation from a partner

a new baby

significant home renovations

redundancy or job loss

a significant increase or decrease in income

inheritance

sale of business

significant health events (i.e. terminal illness, disability or trauma)

retirement

death of a partner, and

a move to aged care.

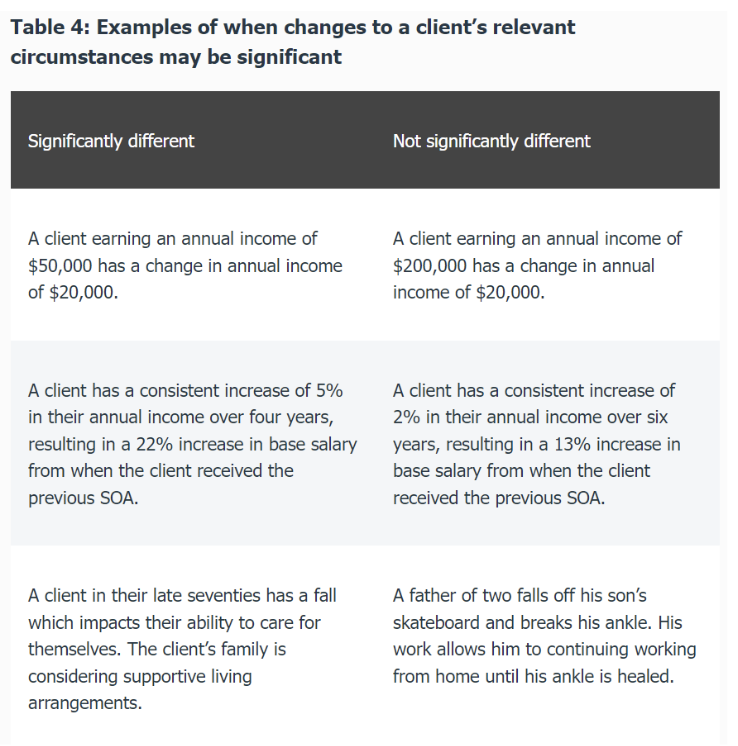

Examples of relevant circumstances that may not be considered significantly different are given in Table 4.

Running the scenario by IIP

We are happy to discuss client scenarios as I can understand that sometimes having someone to talk to and work through a scenario, it can help to clear your mind. But please also be aware that we can’t just bend the rules.

It can be difficult for us to give you definitive clear action. For example, we don’t have access to the previous SOA at the time of the phone call. We also don’t understand your client circumstances in the depth that you do. So, we are only providing guidance based on the information presented to us.

You know your client and previous advice better than anybody else. So, you are in the best position to apply the criteria to the scenario.

Using Scoped Advice

If you do need to provide your client with an SOA, you are able to scope your advice to a single scope.

For example, you previously gave the client an SOA which reviewed the clients superannuation and insurances and gave the client advice on salary sacrifice. The client now wants to make some catch up contributions.

The catch up contributions were not in the previous SOA, there it is new scope and will require an SOA. You do not need to provide advice on the super account and salary sacrifice, etc. You can provide advice simply on the catch-up contributions and scope out the other areas.

What resource do I have available to help make a decision?

The legislation and ASIC Guidance don't necessarily cover all possible client scenarios of when an ROA is appropriate. ASIC encourages advisers to use their professional judgement when applying the guidance to the client scenario.

To help you make a decision, you can refer to the following resources:

ASIC’s Further Advice Guidance: https://asic.gov.au/regulatory-resources/financial-services/giving-financial-product-advice/faqs-records-of-advice-roas/#:~:text=Note%202%3A%20In%20'further%20advice,this%20information%20in%20the%20ROA.

You can also access the IIP Further Advice policy in the iC2 Compliance Hub app.